Compliance Alert: Highlighting Recent Regulatory Changes FEMA Begins Risk Rating 2.0 Flood Insurance Initiative

The Federal Emergency Management Agency (FEMA) provides flood insurance through the National Flood Insurance Program (NFIP),1 which borrowers and lenders can use to satisfy the flood insurance purchase requirements of the Flood Disaster Protection Act of 1973 (FDPA)2 for certain secured loans in special flood hazard areas. FEMA currently has more than 5 million flood insurance policies in force in the United States through the NFIP.3

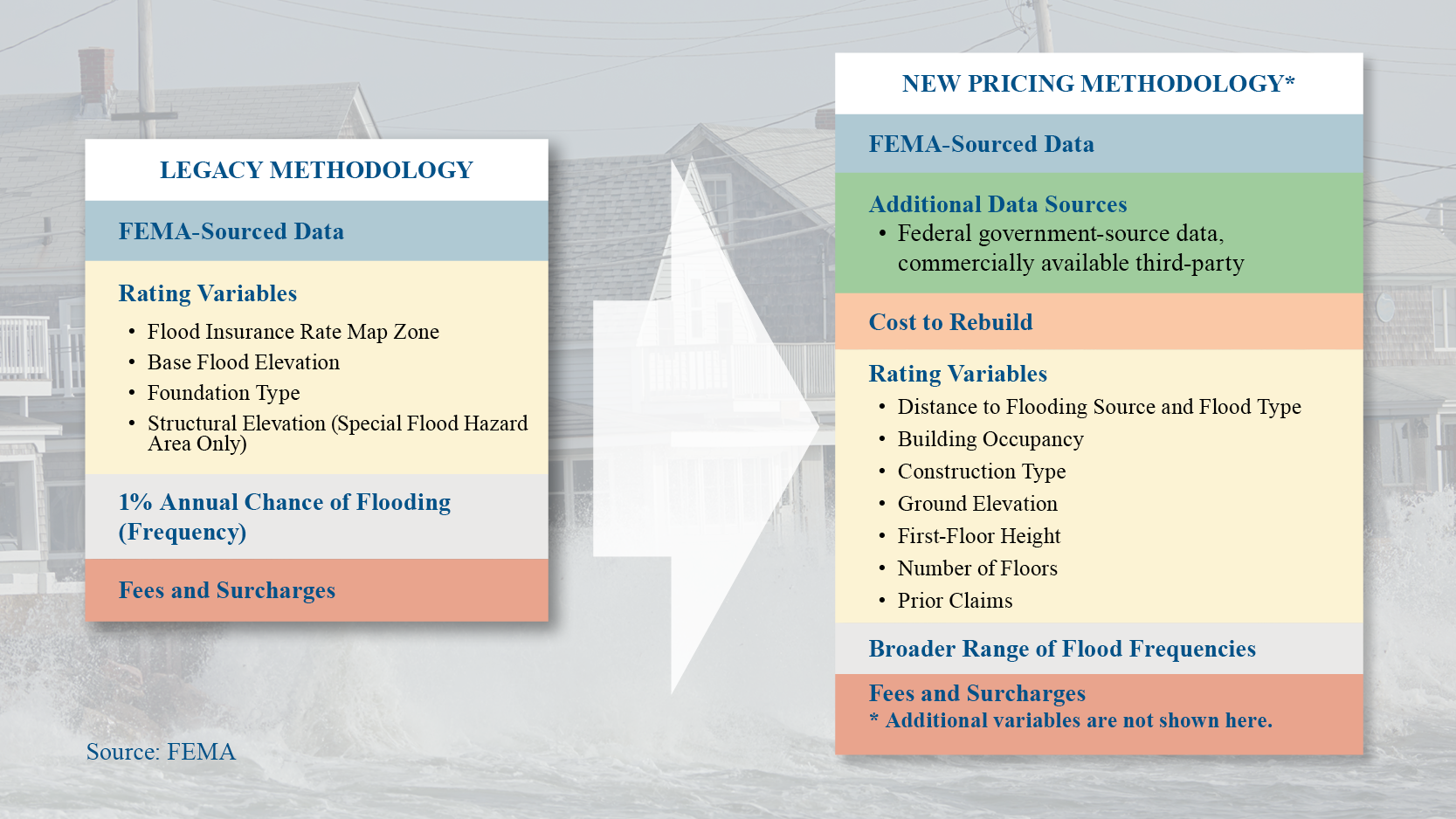

FEMA initiated the Risk Rating 2.0 (RR2) program to more accurately price flood insurance risk. Since the 1970s, FEMA has used a limited number of static measures to determine a property’s risk of flooding, “emphasizing a property’s elevation within a zone on a Flood Insurance Rate Map (FIRM).”4 FEMA determined that this methodology misprices the actuarial risk of a flood, with some insureds paying too much in premiums for their properties, relative to the flood risk, while others are not paying enough.

Risk Rating 2.0 Methodology

In contrast to the legacy methodology, RR2 considers many individual variables in pricing policies, including:

- Frequency of flooding;

- Distance to a water source (such as an ocean or river);

- Property’s elevation;

- Cost to rebuild;

- Number of floors; and

- Different types of floods, such as river overflow, storm surge, coastal erosion, and heavy rainfall.

Figure 1 compares the new factors that FEMA will consider in RR2 with the prior factors in the legacy methodology:

Figure 1: Legacy versus New Pricing Methodology for RR2

|

FEMA uses the tagline Equity in Action for RR2 to emphasize that its revised methodology will help ensure more equitable pricing because flood insurance premiums will more closely align with a property’s individual flood risk. To that end, RR2 eliminates pricing based on flood insurance zones. FEMA noted that within the same flood insurance zone, the risk of a flood can vary. For example, a property close to a water source may have a greater risk of flooding than another property in the same zone that is much farther away from the water source.

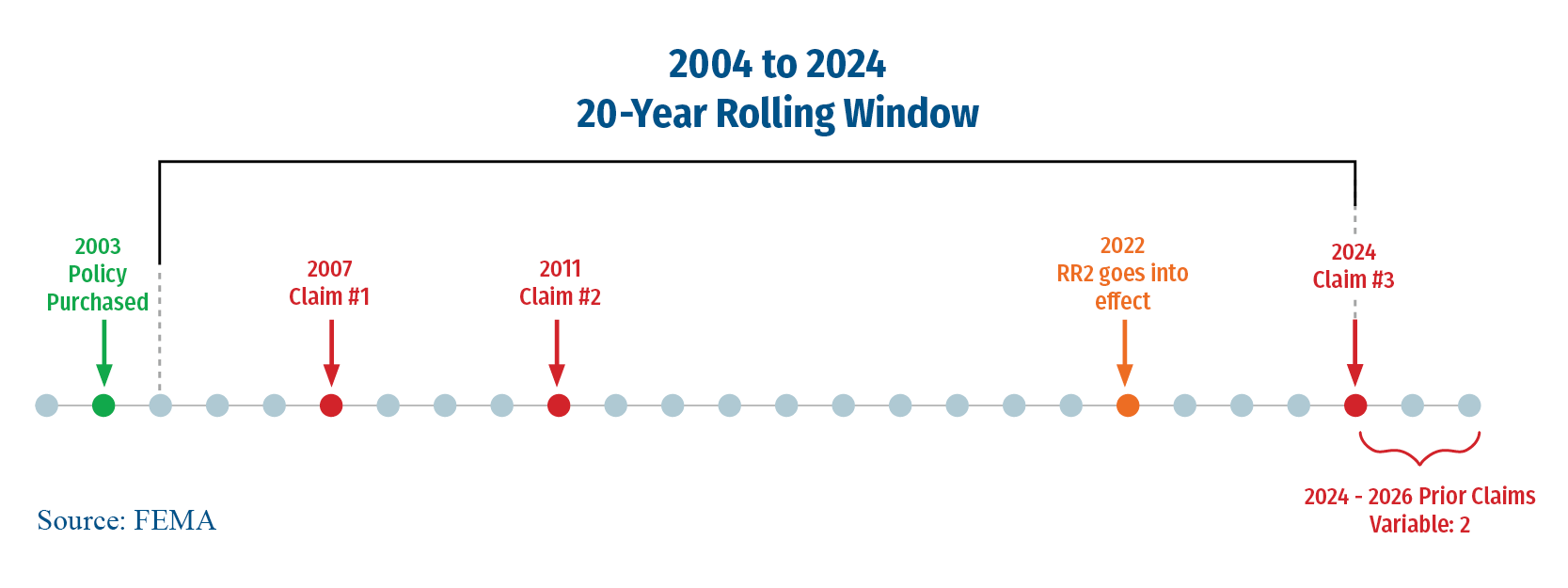

Effect of Prior Claims

When a legacy policy comes up for renewal under RR2, FEMA will not consider the property’s prior paid claims in its initial rate calculation. However, if a claim is filed when the RR2 policy is in effect, FEMA will consider claims paid during the prior 20 years when the policy comes up for renewal (see Figure 2). FEMA provides this example to illustrate how prior claims can impact the rate: A legacy policy was originally issued in 2003, with claims paid in 2007 and 2011. When the policy is renewed under RR2 in 2022, the two claims are not considered. After a claim is filed in 2024, all prior claims since 2004 (a 20-year lookback period) are considered when pricing the renewal of the RR2 policy.5

Figure 2: RR2 Rating Variables, from 2004 to 2024

State Profiles

FEMA has created state profiles that analyze how RR2 will affect rates in all 50 states and the Virgin Islands, including detailed rate examples in spreadsheets at the zip code and county levels.6

Other changes

FEMA is phasing out the following features of the NFIP:

- Grandfathering — For properties with policies in effect when a new flood insurance rate map (FIRM) becomes effective, or were built in compliance with a FIRM when constructed, FEMA allowed the insured to retain the prior rate.

- Submit-for-Rates — For buildings for which no risk rate is published, the property owner could submit an application for a rate.

- Preferred Risk Policies —FEMA offered a lower-cost policy for properties in certain flood zones.

- Mortgage Portfolio Protection Program (MPPP) — FEMA offered force-placed insurance policies through the MPPP.

FEMA is retaining these features of the NFIP:

- Ability to transfer discounts by assigning a policy to a new property owner;

- Current policy limits; and

- Waiving the 30-day waiting period for new loans.

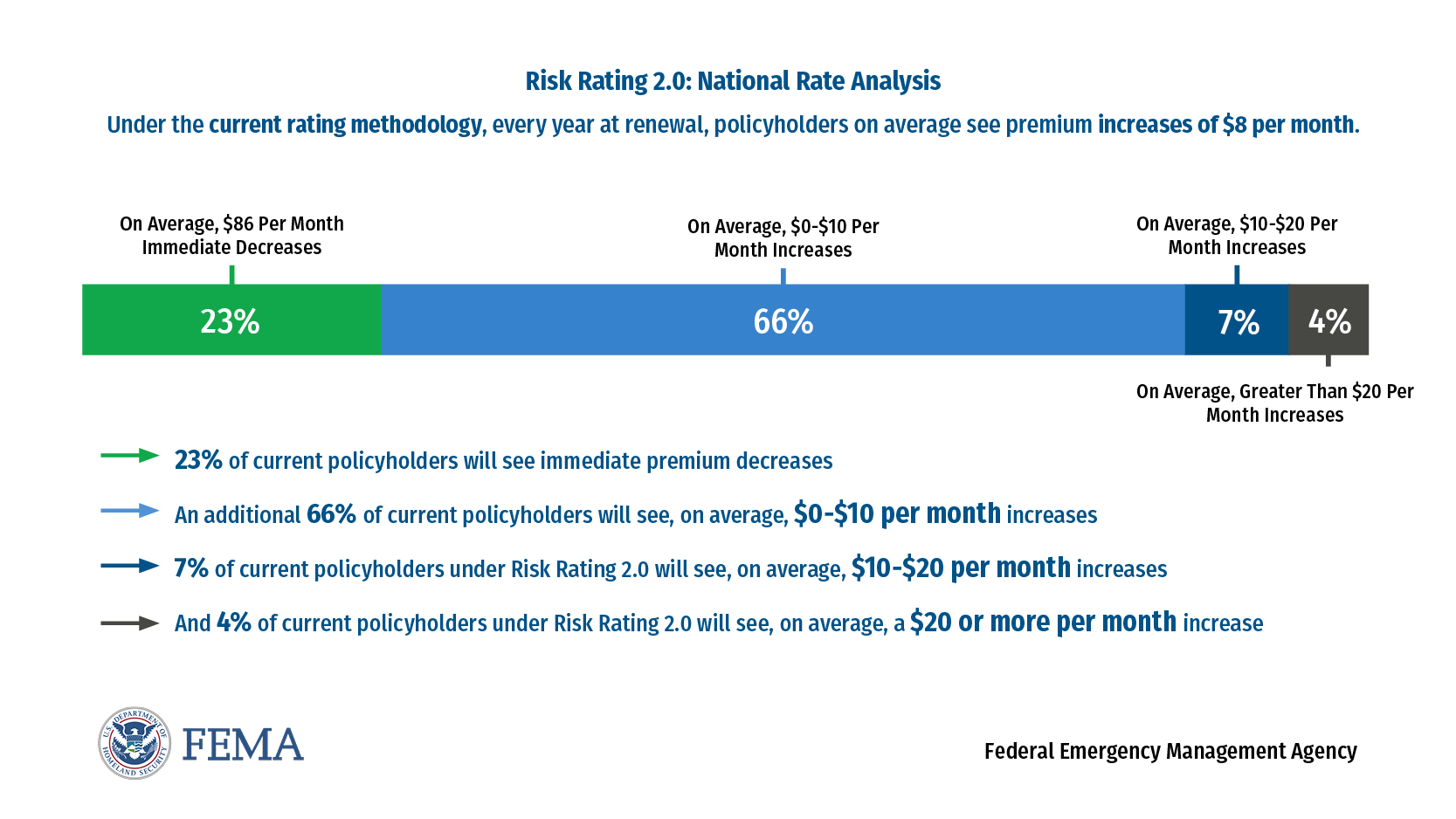

Effect on Premiums

FEMA estimates that 23 percent of policyholders nationwide will see a decrease in premiums, effective at renewal, while all others will see an increase. The Homeowner Flood Insurance Affordability Act (HFIAA) generally limits annual increases in food insurance premiums to no more than 18 percent for individual policies.7 HFIAA imposes a higher annual limit increase of 25 percent for the following properties:

- Nonprimary residences;

- Properties with severe repetitive loss;

- Properties with substantial damage or substantial improvement after July 6, 2012;

- Business properties; and

- Properties with substantial cumulative damage.8

While the annual limits in HFIAA prevent immediate implementation of full risk pricing for policies whose premiums are increasing, premiums will eventually rise to full risk pricing over time. FEMA created an infographic (Figure 3) to display the expected pricing changes:

Figure 3: Expected Pricing Changes for Risk Rating 2.0

Effective Dates

RR2 was effective on October 1, 2021, for all new policies. Existing policies renewing between October 1, 2021, and March 31, 2022, can renew under RR2 or the legacy rating plan. RR2 will apply to all remaining policies renewing on or after April 1, 2022.

Here are several resources for more information:

- FEMA: Risk Rating 2.0: Equity in Action

- FEMA States Flood Insurance Profiles

- Presentation slides for FEMA’s November 2021 webinar on Risk Rating 2.0

- “National Flood Insurance Program: The Current Rating Structure and Risk Rating 2.0” (Congressional Research Service, updated on November 2, 2021)

ENDNOTES

1 See FEMA National Flood Insurance Program.

2 Codified, as amended, at 42 U.S.C. § 4012a.

3 See Watermark Report Fiscal Year 2021 Quarter 1.

4 See FEMA Risk Rating 2.0.

5 FEMA’s presentation slides for its November 30, 2021, RR2 webinar at slide 21.

6 See FEMA Risk Rating 2.0 State Profiles

8 See 42 U.S.C. §4015(e)(4).