Understanding Finance Charges for Closed-End Credit

“The finance charge is the cost of consumer credit as a dollar amount. It includes any charge payable directly or indirectly by the consumer and imposed directly or indirectly by the creditor as an incident to or a condition of the extension of credit. It does not include any charge of a type payable in a comparable cash transaction.” — Regulation Z, 12 C.F.R. §1026.4(a)

The Truth in Lending Act (TILA) requires creditors to disclose key information about consumer credit transactions “so that the consumer will be able to compare more readily the various credit terms available” and “avoid the uninformed use of credit. …”1 The finance charge disclosure informs consumers about the cost of credit expressed as a dollar amount.2 It is also used in calculating other TILA disclosures, including the annual percentage rate (APR). Accurately computing and disclosing the finance charge is important because consumers may rely on it as well as related disclosures whose calculations are based on it, particularly the APR, when shopping for credit and evaluating credit offers. In addition, inaccurate finance charge and APR disclosures can result in restitution to the consumer if the errors exceed regulatory tolerances and can trigger the right of rescission in mortgage transactions subject to rescission.3

Despite the importance of the finance charge disclosure, violations continue to be frequently cited during Federal Reserve examinations.4 To facilitate compliance, this article reviews the regulation’s requirements for determining when a charge must be included in the finance charge, identifies common pitfalls, and offers tips and tools to assist lenders with avoiding and detecting finance charge violations.

Although the definition of a finance charge disclosure is the same for closed- and open-end credit transactions, the disclosure rules are different. This article will focus solely on the disclosure of finance charges for closed-end credit transactions, which are among the violations most frequently cited. The intent of this article is not to provide an exhaustive list of charges qualifying as finance charges under Regulation Z but to review the general principles for determining when a charge is a finance charge for closed-end credit.

IDENTIFYING FINANCE CHARGES

Section 1026.4(a) of Regulation Z defines a finance charge as “the cost of consumer credit as a dollar amount. It includes any charge payable directly or indirectly by the consumer and imposed directly or indirectly by the creditor as an incident to or a condition of the extension of credit. It does not include any charge of a type payable in a comparable cash transaction.”

While on its face this definition seems clear, it can be challenging to apply because of the wide range of fees and charges that can be incurred in credit transactions and because the definition is subject to several exceptions.

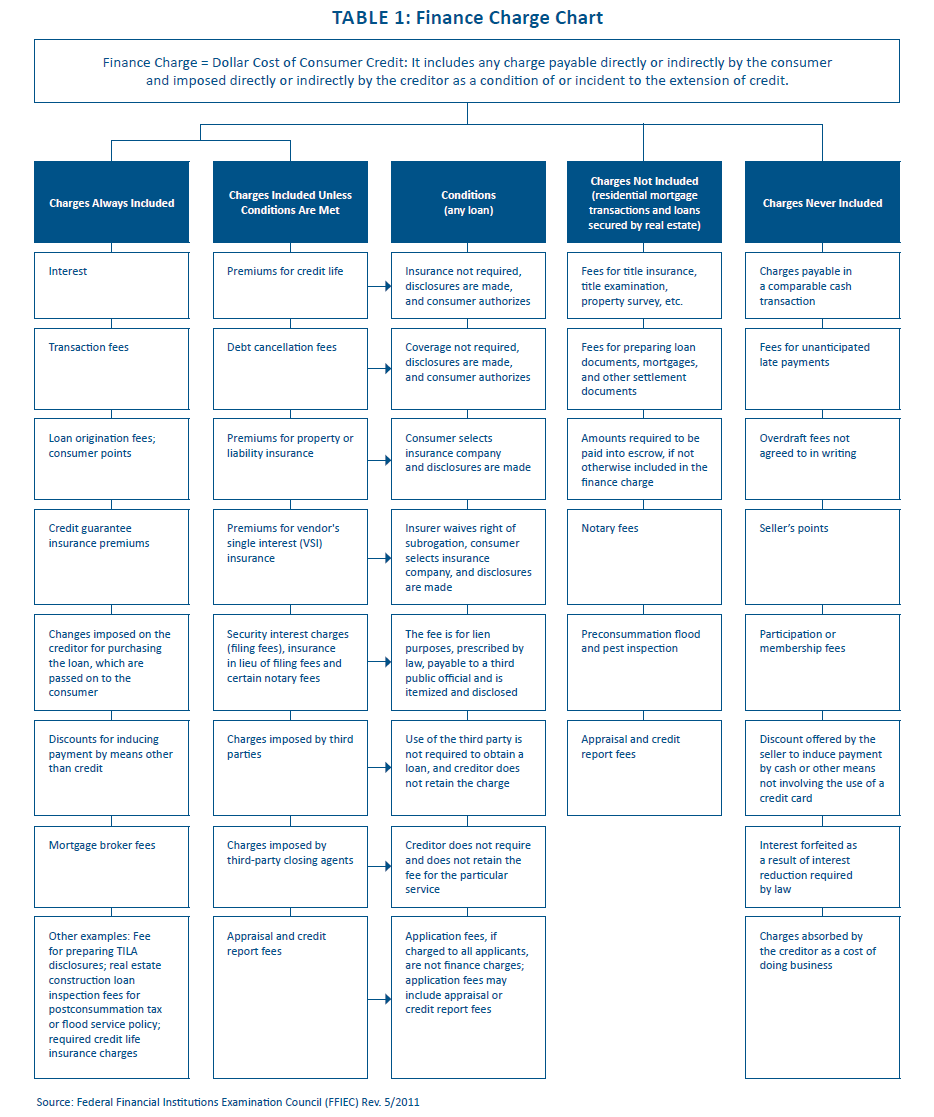

Table 1 displays the “Interagency Examination Procedures for Regulation Z,” which lenders may find helpful for identifying finance charges. That said, the chart and this article are instructive but meant only as a guide. Neither is exhaustive nor exclusive, nor does either substitute for the regulation or Official Staff Commentary (commentary). The chart categorizes charges into several categories: 1) some charges that are always included in the finance charge, 2) some that are always excluded, 3) some that may be excluded if certain conditions are met, and 4) some that are excluded with respect to credit secured by real property or in a residential mortgage transaction (even though they would be considered finance charges in other types of credit transactions). We use this framework for thinking about how charges should be included in the finance charge and when to exclude them.

FINANCE CHARGE RULES FOR CLOSED-END CREDIT

Charges Always Included

A key aspect of the finance charge definition quoted previously is that it captures charges borrowers incur only when they are financing their purchase instead of paying cash.5 Interest is the most obvious example and most common finance charge. Other charges that always qualify include, but are not limited to:

- Loan origination fees6

- Mortgage broker fees7

- Transaction fees8

- Discount for inducing payment without using credit9

- Borrower-paid points10

- Credit guarantee insurance premiums11

- Construction loan inspection fees12

- Fees imposed, regardless of when collected, for services performed periodically during the loan term in connection with a real estate or residential mortgage transaction such as tax lien searches or flood insurance policy determinations13

Charges Never Included

Regulation Z and the commentary provide examples of charges that are never finance charges because they are not incident to, or a condition of, an extension of credit, or because they are imposed uniformly on credit and cash transactions:

- Charges for an unanticipated late payment, for exceeding a credit limit, or for delinquency, default, or a similar occurrence are not finance charges14

- Seller’s points

- Taxes, license fees, or registration fees paid by both cash and credit customers are generally not finance charges.15 However, a tax imposed by a state or other governmental body solely on a creditor (not the consumer) that the creditor separately imposes on the consumer is a finance charge.16 Also, to the extent a charge imposed by a creditor exceeds the same charge in a comparable cash transaction, the difference is a finance charge.17

- When a borrower is required to purchase an item or service in a credit transaction, but that item or service is not required in a comparable cash transaction, the charge would be a finance charge, even if the item or service may be voluntarily purchased by a consumer paying cash. For example, if a lender required the purchase of a maintenance or service contract in a credit transaction, the charge would be a finance charge even though cash customers in that scenario have the option of purchasing such a contract.18

Charges Included Unless Conditions Met

In three different categories — third-party fees, insurance premiums and fees for debt cancellation/debt suspension coverage, and security interest fees — charges are included in the finance charge unless certain conditions are satisfied.

THIRD-PARTY FEES

In some credit transactions, particularly secured ones, consumers may incur charges for services provided by third parties, such as a courier service, that are not otherwise payable in a comparable cash transaction. The regulation generally includes these third-party charges in the finance charge (when not expressly excluded elsewhere), if the creditor either:

- requires the use of the third party as a condition of or an incident to the extension of credit, even if the consumer can choose the particular third party; or

- retains a portion of the third-party charge (and if it does retain a portion, that portion is a finance charge).19

If neither of these conditions apply, the third-party charges may be excluded from the finance charge.

A separate rule applies for charges by a third-party closing agent (such as a settlement agent, attorney, or escrow or title company). These charges are included in the finance charge if the creditor: 1) requires the particular service for which the fee is incurred, 2) requires the charge be imposed, or 3) retains a portion of the charge (if a portion is retained, that portion is a finance charge).20 Similar to the third-party charges described previously, if none of these circumstances apply, the charge may be excluded from the finance charge. Comment 4(a)(2)-1 of the commentary to Regulation Z provides as an example that a courier fee would be included when the creditor requires the use of a courier. (See also the discussion about lump sum closing charges.)

Special Rule for Borrower-Paid Mortgage Broker Fees

Borrower-paid mortgage broker fees are finance charges even if the creditor does not require the consumer to use the broker and does not retain any portion of the charge.21

INSURANCE AND DEBT CANCELLATION AND DEBT SUSPENSION COVERAGE

In the case of a charge on premiums for certain types of voluntary insurance, such as credit life, accident, health, and loss-of-income, and premiums charged for voluntary debt cancellation or suspension coverage (whether or not the coverage is considered insurance), the charge may be excluded from the finance charge if the following conditions are satisfied:

- The insurance or coverage is not required by the creditor and is disclosed in writing.

- The consumer is provided the written disclosure for the particular insurance or coverage required by §1026.4(d)(1)(ii) or §1026.4(d)(3)(ii) and (iii).

- The consumer affirmatively elects the insurance or coverage.22 To evidence consent, the consumer must sign or initial an affirmative written request for the insurance or coverage after receiving the required disclosures. In the case of telephone purchases, the creditor must make the disclosures orally, send printed copies within three business days, and maintain records that the consumer elected to purchase the insurance or coverage after receiving the disclosures.

Property insurance premiums may also be excluded from the finance charge if the consumer can choose the insurer and this option is disclosed.23 Additional disclosures regarding premiums and the terms of insurance are required if the insurance is obtained from or through the creditor.24

These same rules apply to a vendor’s single interest (VSI) insurance but only if the VSI insurer waives all rights of subrogation against the consumer.25

CERTAIN SECURITY INTEREST CHARGES

The following charges incurred for a security interest in the collateral securing a loan may also be excluded from the finance charge if the charges are itemized and disclosed:

- Taxes and fees prescribed by law that actually are or will be paid to public officials for determining the existence of or for perfecting, releasing, or satisfying a security interest; alternatively, the premium for insurance in lieu of perfecting a security interest may be excluded to the extent it does not exceed the amount of such fees that would otherwise be payable.

- Any tax levied on security instruments or on documents evidencing indebtedness if the payment of such taxes is a requirement for recording the instrument securing the evidence of indebtedness.26

Real Estate-Related Fees

Regulation Z applies a special rule that excludes five types of charges from the finance charge in a residential mortgage transaction27 or a real estate-secured loan, provided the charges are both bonafide and reasonable:

- Fees for title examination, abstract of title, title insurance, property survey, and similar purposes

- Fees for preparing loan-related documents, such as deeds, mortgages, and reconveyance or settlement documents

- Notary and credit-report fees

- Property appraisal fees or fees for inspections to assess the value or condition of the property if the service is performed prior to closing, including fees related to pest-infestation or flood-hazard determinations

- Amounts required to be paid into escrow or trustee accounts if the amounts would not otherwise be included in the finance charge28

As noted in the commentary, these fees are excluded from the finance charge even if the creditor’s employees, rather than a third party, perform the services for which the fees are imposed.29 The cost of verifying or confirming information connected to an excludable item is also excludable. For example, credit-report fees cover not only the cost of the report but also the cost of verifying information in the report.30

When a lump sum is charged for several services, any portion attributable to a nonexcludable charge should be allocated to that service and included in the finance charge. However, the staff commentary notes that if a lump sum is charged for conducting or attending a closing and the charge is primarily for services related to items listed in §1026.4(c)(7), the entire charge is excluded even if a fee for incidental services provided (such as explaining various documents or disbursing funds for the parties) would be a finance charge if it were imposed separately.31

Finally, the charges under §1026.4(c)(7) for consumer loans secured by real estate and residential mortgage transactions are excludable only when imposed solely in connection with the initial decision to grant credit. For example, as noted previously, a fee for one or more determinations during the loan term of the current tax-lien status or flood-insurance requirements is a finance charge, regardless of whether the fee is imposed at closing or when the service is performed.

The commentary states the entire fee may be treated as a finance charge if a creditor is uncertain about what portion of a fee paid at consummation or loan closing is related to the initial decision to grant credit.32

DISCLOSURE REQUIREMENTS AND TOLERANCES

Finance Charge Disclosure in Closed-End Transactions

While this article focuses on identifying and disclosing the finance charge, it is important to recognize that errors in determining the finance charge can contribute to errors in other TILA disclosures that rely upon an accurate finance charge.

In any closed-end credit transaction, TILA requires disclosure of the total finance charge, which is the sum of all charges, expressed as a dollar amount, that meet the regulatory definition of finance charge. For consumer closed-end real-estate secured loans (i.e., loans subject to the CFPB’s TILA-RESPA integrated disclosure rule that went into effect in October 2015), the finance charge must be disclosed on page 5 of the “Closing Disclosure,” as required by §1026.38(o)(2). For other closed-end loans, §1026.18(d) provides for disclosure of the finance charge, using that term, and a brief description such as “the dollar amount the credit will cost you.” The APR is also calculated based on the finance charge. Excluding charges from the finance charge that should have been included will result in an understated APR, which makes the APR appear lower than it actually is.

Regulatory Tolerances

Regulation Z defines tolerances with respect to the disclosed finance charge. For closed-end loans, the tolerances appear in Section 1026.18(d).

Mortgage loans:33

- understated by no more than $100, or

- greater than the amount required to be disclosed.

Other credit:

- If the amount financed is $1,000 or less, the finance charge cannot be more than $5 above or below the amount required to be disclosed.

- If the amount financed is greater than $1,000, the finance charge cannot be more than $10 above or below the amount required to be disclosed.

Inaccurate disclosure of the finance charge and APR outside of tolerances can result in restitution to consumers affected by such errors.

COMMON ISSUES, TIPS, AND TOOLS

Common Issues

Properly classifying fees as finance charges can be challenging, and errors can be costly. Common issues Federal Reserve examiners have seen that result in finance charge errors include:

- Not accounting for all charges — Lenders should ensure that they consider every charge paid by a consumer when determining the total finance charge; in other words, each charge should be clearly identified as either a finance charge or not a finance charge. Errors may occur because the lender failed to evaluate whether or not the charge was a finance charge.

- Mischaracterizing charges — The service for which a charge is incurred, not the name of the service, determines if it is a finance charge. For example, calling a loan origination fee a “processing” fee does not change the nature of the charge; it would still be a finance charge.

- Failure to meet the requirements for “conditional” exclusions — Another source of error is excluding charges from the finance charge even though the conditions to exclude the charge have not been met. For example, not having a customer sign or initial an affirmative election of credit life insurance as required would make the cost of the insurance a finance charge.

- Payments to third parties — A creditor may mistakenly believe that if it does not retain a charge collected on behalf of a third party, it is not a finance charge. Charges paid to third parties can be excluded if the use of the third party is not required to obtain the loan and the creditor does not retain a portion of the charge. However, in some cases, charges paid to third parties are excluded only if certain conditions are met, such as making required disclosures about the charge and the voluntary nature of the charge. Finally, some charges paid to third parties, such as credit guarantee insurance premiums and mortgage broker fees, are always finance charges.

- Automated systems — The use of automated loan and disclosure systems can facilitate compliance; however, creditors must understand how these systems function. This understanding helps ensure the creditor properly sets system parameters and inputs accurate information into the system. Many systems require an initial set-up, which may require the user of the system to correctly identify which charges are finance charges. Once set up correctly, a properly functioning system can produce consistently accurate disclosures. However, errors in the set-up process; changes in a lender’s practices, such as introducing new charges; or system updates/changes can result in a system that produces erroneous disclosures.

Tips and Tools

Creditors can employ a number of techniques to prevent finance charge violations, including the following:

- Train staff and provide tools, such as the chart, to help with accurately recognizing, classifying, and disclosing finance charges. It is important to remember, though, that the chart provides a high-level guide to the regulatory requirements (as do other tools or job aids) but is not a substitute for the regulation or the commentary.

- Establish processes for trained staff to evaluate all charges associated with all consumer loan products to determine which charges are finance charges and which are not. These processes should be repeatable so that as lender practices change over time, such as with the introduction of new charges or new products, finance charges are correctly identified and disclosed.

- Use automated systems that correctly capture and disclose finance charges. The systems should also accurately factor finance charges into the computation and disclosure of items related to the finance charge, such as the amount financed. If a creditor imposes a new fee, it should be vetted to determine if it is a finance charge. Verify system settings periodically/routinely and test them after any update or change.

- Review loan disclosures, including the finance charge, for accuracy when initially setting up a loan and during periodic testing.

CONCLUSION

Although the definition and treatment of finance charges have not changed in recent years, finance charge errors for closed-end loans remain a source of frequent violations and can result in restitution to affected borrowers. By taking a step back and looking at the charges using a methodical process, creditors can enhance controls to mitigate potential risk. Ensuring that staff is appropriately trained and that disclosure systems are up to date and accurate will help prevent disclosure errors. Routine testing processes will allow creditors to detect and correct any errors. Specific issues and questions should be raised with your primary regulator.

Endnotes

1 15 U.S.C. §1601

2 12 C.F.R. §1026.4(a)

3 15 U.S.C. §1607(e) (restitution); 12 C.F.R. §1026.23(a)(3)(i) and (ii) (the finance charge and the APR are two material disclosures that trigger right of rescission for up to three years after consummation if they are inaccurate).

4 The Federal Reserve Board examines state-chartered banks that are members of the Federal Reserve System with assets of $10 billion or less to ensure compliance with federal consumer protection laws, including Regulation Z. As of February 2017, the number of such banks was 830.

5 12 C.F.R. §1026.4(a)

6 12 C.F.R. §1026.4(b)(3)

7 12 C.F.R. §1026.4(a)(3)

8 12 C.F.R. §1026.4(b)(2)

9 12 C.F.R. §1026.4(b)(9). The commentary provides this example: A tract of land is sold for $9,000 if paid in cash, but $10,000 if financed. The $1,000 difference is a finance charge if the purchase is financed. Comment 4(b)(9)-1.

10 12 C.F.R. §1026.4(b)(3)

11 12 C.F.R. §1026.4(b)(5)

12 Comment 4(a)-1.ii.A ![]()

13 12 C.F.R. § 1026.4(c)(7) and Comment 4(c)(7)-3

14 12 C.F.R. §1026.4(c)(2)

15 Comment 4(a)-1.i.A

16 Comment 4(a)-5.i.A

17 Comment 4(a)-1.iii

18 Comment 4(a)-1.ii.C

19 12 C.F.R. §1026.4(a)(1)

20 12 C.F.R. §1026.4(a)(2)

21 12 C.F.R. §1026.4(a)(3)

22 12 C.F.R. §1026.4(d)(1) and (d)(3)

23 12 C.F.R. §1026.4(d)(2)

24 12 C.F.R. §1026.4(d)(2)(ii)

25 12 C.F.R. §1026.4(d)(2)

26 12 C.F.R. §1026.4(e)

27 This is defined in §1026.2(a)(24) ![]()

![]() as a credit transaction secured by the consumer’s principal dwelling to finance the purchase or initial construction of the dwelling.

as a credit transaction secured by the consumer’s principal dwelling to finance the purchase or initial construction of the dwelling.

28 12 C.F.R. §1026.4(c)(7)

29 Comment 4(c)(7)-1

30 Comment 4(c)(7)-1

31 Comment 4(c)(7)-2

32 Comment 4(c)(7)-3

33 These tolerances apply to loans secured by real property or a dwelling. These same tolerances apply to loans secured by real property subject to §1026.38 as set forth in §1026.38(o)(2). ![]()

![]()