RESPA Part Two: Changes to the HUD-1 Form

Congress enacted the Real Estate Settlement Procedures Act (RESPA) in 1974 “to ensure that consumers throughout the Nation are provided with greater and more timely information on the nature and costs of the settlement process and are protected from unnecessarily high settlement charges caused by certain abusive practices that have developed in some areas of the country.”1 In November 2008, the United States Department of Housing and Urban Development (HUD) published a final rule2 to amend Regulation X, RESPA’s implementing regulation, to ensure more timely and effective disclosures of the settlement costs of residential mortgage loans.3 The amendment significantly changed RESPA’s two primary disclosure forms: the Good Faith Estimate (GFE) and the HUD-1 settlement statement. The changes were effective January 1, 2010.

HUD revised the HUD-1 disclosures to facilitate comparison between the GFE, which loan originators must provide to borrowers within three business days after application, and the HUD-1, which settlement agents must provide to borrowers at or before closing. To accomplish this objective, HUD-1’s terminology was modified to conform to the GFE’s terminology. Also, a final page was added to the HUD-1 that provides a summary of the loan terms and a Comparison Chart that displays the settlement charges from the GFE and the HUD-1 in a tabular format. The Comparison Chart allows the borrower to easily determine whether the estimate of settlement charges disclosed at application in the GFE exceed the actual charges disclosed on the HUD-1 at closing by more than the permitted tolerances.

This article is the second in a two-part series dealing with HUD’s amendments to Regulation X. Part one, “RESPA Changes to the Good Faith Estimate Form,” which was published in the Second Quarter 2010 issue of Consumer Compliance Outlook, reviewed two important changes to the GFE: (1) changed circumstances and (2) tolerance and cure.4 Part two addresses three important facets of the HUD-1: (1) determining when to use the HUD-1/1A; (2) disclosing charges paid outside of closing (P.O.C.); and (3) curing tolerance violations.

DETERMINING WHEN TO USE THE HUD-1/1A

RESPA directed HUD to develop a standard form to disclose settlement costs, and HUD responded with the HUD-1 and HUD-1A forms. The HUD-1 is the standard three-page form settlement agents must use for all federally related mortgage loans involving a borrower and a seller.5 The HUD-1A is a two-page optional form that “may be used for refinancing and subordinate lien federally related mortgage loans, as well as for any other one-party transaction that does not involve the transfer of title to residential real property.”6 However, the regulation also permits such one-party transactions to be recorded by completing the borrower’s side of the HUD-1.7 Given the overlap between the HUD-1 and HUD-1A, Regulation X often references the two forms as a single form, the HUD-1/1A.

The HUD-1/1A must be used for every RESPA-covered transaction unless specifically exempted.8 The only specific exemption is in §3500.8(a) for an open-end home equity line of credit covered by the Truth in Lending Act and Regulation Z. Although the HUD-1/1A is not required for certain transactions, HUD specifically states in its Instructions for Completing HUD—1 and HUD—1A Settlement Statements (HUD-1 Instructions) that it does not object “to the use of the HUD—1 in transactions in which its use is not legally required.”9 The instructions even encourage the use of the HUD-1A for open-end lines of credit transactions. It is important to note that using the HUD-1/1A in a transaction otherwise not covered by RESPA “does not subject a transaction to coverage under RESPA.”10

DISCLOSING CHARGES PAID OUTSIDE OF CLOSING

Any settlement charges paid before or after closing are considered “paid outside of closing” (P.O.C.) and are disclosed on the HUD-1 differently from settlement charges paid at closing. Settlement charges paid at closing are listed on the appropriate line of the HUD-1 and included in the Borrower’s and Seller’s columns. While P.O.C. charges are still disclosed on the appropriate line of the HUD-1, they are labeled P.O.C. and recorded outside of the Borrower’s and Seller’s columns.11

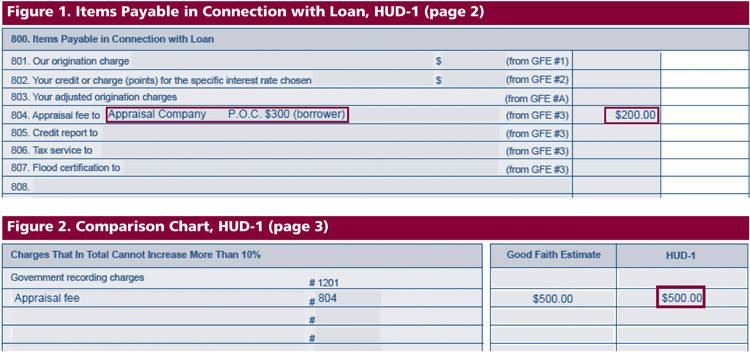

To properly record a P.O.C. charge, the settlement agent must identify the amount of the payment and who made it.12 For example, suppose appraisal services cost $500, but the borrower is paying $300 with earnest money. In Line 804, the settlement agent records the $300 paid outside of closing outside of the columns as “Appraisal Company P.O.C. $300 (borrower)” and places the remaining balance ($200) inside the Borrower’s column. (See Figure 1.13) When computing the “Total Settlement Charges” on line 1400, only the amount listed in the columns on Line 804 — not the P.O.C. amount listed outside the columns on Line 804 — should be included in the total.

For the Comparison Chart on the last page of the HUD-1, the settlement agent recombines the amount identified as P.O.C. by the borrower ($300) and the amount in the Borrower’s column ($200) to obtain the correct value for the Comparison Chart ($500), as shown in Figure 2.14

HUD’s changes to Regulation X were driven, in large part, by HUD’s goal of improving the disclosure of yield spread premiums (YSPs) “to help borrowers understand how YSPs can affect borrowers’ settlement charges.”15 HUD’s main concern was that YSPs were often used for the originator’s benefit rather than to help the consumer offset origination and settlement costs. To more clearly identify YSPs and other indirect payments from the lender to the mortgage broker, the FAQs state that such payments should not be recorded as P.O.C.16 Instead, these payments must be disclosed on Line 802 as a credit to the borrower and recorded outside of the Borrower’s column.17 If the borrower pays a portion of the origination charge before settlement, an offsetting credit is disclosed on Lines 204 — 209 of the HUD-1.18

CURING TOLERANCE VIOLATIONS

Once the Comparison Chart is completed, the lender and settlement agent will check for tolerance violations. The tolerances create limits on the extent to which the actual settlement charges can exceed the amounts disclosed on the GFE.19 The RESPA final rule establishes three categories of settlement charges, with different tolerances for each category. A chart identifying the charges contained in each category can be found on the last page of the GFE. The three tolerance categories are:

- Charges That Cannot Increase: The origination charge, credit charge, adjusted origination charges, and transfer taxes have a zero tolerance.

- Charges That in Total Cannot Increase More Than 10 Percent: The government recording charges, title services, lender’s title insurance, owner’s title insurance, and any other required services that are provided by a company identified by the loan originator cannot increase by more than 10 percent in the aggregate. Any individual charge may exceed 10 percent so long as the sum of the charges remains below the 10 percent threshold.20 Only service providers identified by the loan originator are required to be included in this category.21 A loan originator might identify a service provider either orally or in writing. However, if the consumer purchases required services from a provider not identified by the loan originator, these settlement costs would fall under the “charges that can increase” category.

- Charges That Can Increase: The initial escrow deposit, daily interest charges, homeowner’s insurance, and any required services consumers purchase from providers not identified by the loan originator have no tolerance restrictions.

If a charge exceeds the permitted tolerances, §3500.7(i) provides that the loan originator has 30 calendar days from the date of settlement to “cure” the violation by reimbursing the borrower the amount by which the tolerance was exceeded. Because of this 30-day window to cure a violation, the settlement agent does not have to stop a closing solely because of a tolerance violation.22

Curing a tolerance violation involves: (1) reimbursing the borrower and (2) revising the HUD-1. It is the loan originator’s responsibility to reimburse the borrower the amount by which the actual settlement charges exceed the permitted tolerances.23 Although the loan originator is responsible for reimbursement, the loan originator may authorize a third party (including the settlement agent) to send the reimbursement to the borrower.24 Even if a seller or person other than the borrower pays for a settlement service, the loan originator or a third party authorized by the loan originator must reimburse the borrower for any tolerance violation that might have occurred.25 Under §3500.7(i), a borrower will be deemed to have received timely reimbursement if the payment is delivered or placed in the mail within 30 days after settlement.

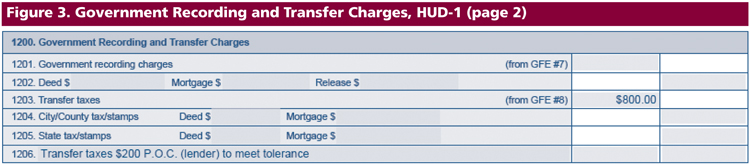

Whenever a tolerance violation is cured, an amended HUD-1 must be issued. It is the loan originator’s responsibility to notify the settlement agent of the changes necessary to correct the HUD-1.26 The amended HUD-1 must state the actual charges paid by the borrower and seller. One way to disclose a violation cure is to correct the amounts listed on page two of the HUD-1 to reflect the actual amount charged to the borrower (i.e., the amount from the initial HUD-1 less the reimbursement).27 On a blank line in the applicable section, the settlement agent should make a notation that the loan originator has made a P.O.C. payment of a specified amount to correct a tolerance violation.28 Figure 3 illustrates how to record a cure of $200 of transfer tax charges.29 Line 1203, which would have listed $1,000 on the original HUD-1, has been reduced to $800 and the $200 has been listed as P.O.C. on Line 1206.

Another way to disclose a cure for a tolerance violation is to list the cure as a credit to the borrower on page 1 of the HUD-1 along with a description of the service to which the credit was applied. The next example from the FAQs involves a cure of $180 for a violation of the 10 percent tolerance category.30 Since the 10 percent tolerance category is an aggregate measure, the cure can be listed as a lump sum amount (see Figure 4).

After the necessary changes have been made, the settlement agent must provide copies of the corrected HUD-1 to the borrower, seller, and loan originator, as appropriate. The settlement agent may mark the amended HUD-1 as “Amended” to distinguish it from the original HUD-1.31

CONCLUSION

HUD revised its regulations to ensure more timely and effective disclosures of mortgage settlement costs for federally related residential mortgage loans. The new regulations altered the terminology in the HUD-1 to better match the GFE and added a third page to the HUD-1 to clearly indicate important loan terms and show differences between settlement charges disclosed on the GFE at application and the final charges disclosed on the HUD-1 at closing.

Part one of this series, published in the Second Quarter 2010 issue of Outlook, discussed important changes to the GFE and began the discussion on tolerances. This article addressed changes in the HUD-1/1A and built on the tolerance discussion, demonstrating how to calculate tolerances and cure tolerance violations. Specific issues and questions should be raised with the consumer compliance contact at your Reserve Bank or with your primary regulator.

- 1 12 U.S.C. §2601(a)

- 2 73 Fed. Reg. 68,203 (November 17, 2008)

- 3 RESPA applies to all “federally related mortgage loans,” as defined in 24 C.F.R. §3500.2(a) . This definition covers almost all transactions involving mortgages securing loans on one- to four-family residential properties.

- 4 Consumer Compliance Outlook: Second Quarter 2010

- 5 24 C.F.R. §3500.8(a)

- 6 HUD-1A Instructions

- 7 24 C.F.R. §3500.8(a)

- 8 24 C.F.R. §3500.8

- 9 The HUD-1 instructions are available at http://edocket.access.gpo.gov/cfr_2010/aprqtr/pdf/24cfr3500AppA.pdf.

- 10 New RESPA Rule FAQs (FAQs) (April 2, 2010), p. 44, Q.2

- 11 Regulation X does not directly address P.O.C. charges. Instead, §3500.8(a) requires that settlement agents complete the HUD-1/1A in accordance with the instructions in Appendix A of the regulation. This appendix addresses P.O.C. charges.

- 12 HUD-1 Instructions

- 13 RESPA FAQs, p. 59

- 14 RESPA FAQs, p. 59

- 15 73 Fed. Reg., p. 68,204

- 16 RESPA FAQs, pp. 31, 49

- 17 The FAQs provide additional guidance on this issue in questions 4 and 5 on p. 49.

- 18 RESPA FAQs, p. 49

- 19 24 C.F.R. §3500.7(e)

- 20 RESPA FAQs, p. 58

- 21 24 C.F.R. §3500.7(e)(2)(ii)

- 22 RESPA FAQs, p. 41

- 23 RESPA FAQs, p. 41

- 24 RESPA FAQs, p. 41

- 25 RESPA FAQs, p. 43

- 26 RESPA FAQs, p. 42

- 27 RESPA FAQs, p. 42

- 28 RESPA FAQs, p. 42

- 29 RESPA FAQs, p. 42

- 30 RESPA FAQs, p. 43

- 31 RESPA FAQs, p. 43